Minor maintenance with a swap of Loudspring for CapMan Plc. Sold the tiny position that consisted of 550 Loudspring shares for 0,338 EUR per share and bought additional 110 CapMan shares for 2,315 EUR per share. This was mainly done because I have some indirect exposure for Loudspring even without this and it’s very likely that I have plenty of time to jump back in should there be significant change on the outlook. Essentially this is is streamlining effort which helps on the process of building a real position on CapMan.

Q4/2019 and FY2019 Results

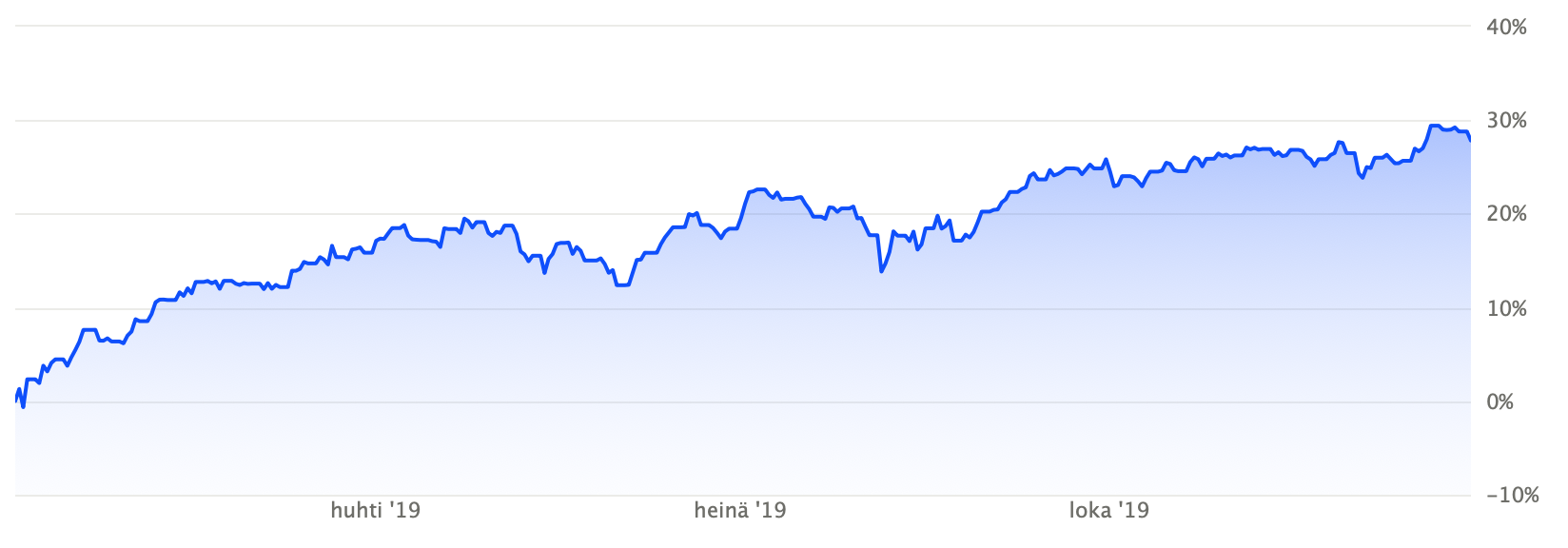

Another eventful year has passed. Global economy had some major setbacks such as the trade war, approaching US presidential elections with the internal issues that comes with it, the ever ongoing BREXIT saga and loads of smaller issues which I’m sure the middle east region will provide us for many years to come. Then there’s the situation with central banks and interest rates. Considering all this it’s really mind blowing to think how well stocks have performed. Portfolio value is really a secondary metric for me but primary portfolio value increased about 28% this year. This is somewhat in-line with index performance but this being an income oriented portfolio, unrealised capital gains are secondary but nice to have of course.

During FY2019 I re-arranged my personal finances and paid of my mortgage. For me this constitutes as the first step of three in the path to financial independence as it reduces significantly the required income for mandatory monthly expenses. In retrospect I probably should’n have sold some of the stocks for this (looking at Apple Inc. especially which has rallied since then) but these investments are done for a purpose and those realised profits filled their purpose in bigger picture. No hard feelings there especially since I very well realised that this could be exactly the outcome even for the Apple share.

Dividend income for FY2019 increased quite nicely compared to previous year. This happened even though I was not buying as aggressively as in year before due to decreased leverage on the portfolio. There were some one time extra dividends (BHP Billiton) and some negative news for next year as some of key positions will decrease the dividends next year (Nordea, Sampo). For FY2020 I expect consistent cash injections and full dividend re-investments which should offset those negatives and keep dividend growth trend in same trajectory. For FY2019 the total dividend income before taxes and converted to euros was 6769 EUR.

In the spirit of traditional new year’s resolutions I’ve set following goals for 2020:

- Personal savings rate of 70%

- Second step on the path to financial independence: passive income covers base consumption

- 12 months without alcoholic beverages

- Protecting effective tax rate (offset increased taxes with tax planning)

Recent Buy: CapMan Plc

First real purchase in the process of building a position on CapMan with a purchase of 320 shares bought for 2,27 EUR per share. More will follow during next few months unless something else comes up. CapMan serves a proxy for quite interesting sectors when we as societies are in the beginning of a major shift. As they but it:

At CapMan, we build better organised, managed, and financially stable companies, because this contributes to overall economic well-being. More jobs and innovations equal better conditions for the society. Similarly, we invest in real estate and infrastructure, because we believe that functional high-quality environments and utilities are cornerstones for functioning societies.

Most of all it is a dividend oriented company and therefore fits into my strategy as a potential combination of high initial yield and decent dividend growth. On top of that I suspect that there might be some real M&A possibilities in coming years which could lead to significant price appreciation. Recent insider activity is also a plus at this point.

Recent Buy: EPR Properties

Dividend re-investment for the portfolio hosted in Nordnet with the purchase of 15 EPR Properties shares. Purchase price was 69,99 USD per share. Not much to say about this one. Still reasonably priced and company profile in general is acceptable considering the phase of the market. There are decent valuations available but it’s very difficult to find anything really interesting to buy at the moment in the dividend scope. Personally I doubt we would be getting a major correction next year but it is possible of course. Political tensions have been pushed back a bit but no doubt will come back at some point especially with the approaching US elections and possible deal with China.

Recent Buy: CapMan Oyj

Tiny maintenance purchase for portfolio hosted in Nordea. CapMan is a position which I intend to build in the coming months or during Q1/2020 but for the “mandatory” at least one transaction per quarter I bought mere 20 shares for 2,045 EUR per share . CapMan will be included in primary portfolio even though hosted in Nordea. I plan to buy some of the primary portfolio holding for the portfolio hosted in Nordea as it will spread the broker risk. Most likely these will be mainly European stocks listed in euros as my primary broker (Nordnet) has accounts for various currencies which allows me to decide when to convert dividends received in various currencies. For now the portfolio hosted in Nordnet will in one kind of maintenance mode (new purchases being mainly dividend re-investments).

Recent Buy: EPR Properties, CoreCivic & GEO Group

It’s been a while since my last real purchase in main portfolio but today there was three. Hopefully this wasn’t motivated by the negative news from Nordea Bank and Sampo. Both of which are slashing next dividend. First purchase was additional 15 shares of EPR properties bought for 79,46 USD per share. Nothing special here. Decent valuation and acceptable company profile given the interest rate environment and phase of the cycle. GEO Group and CoreCivic are much more interesting. Both are in the much hated for profit prison business which has taken a real beating as the US presidential election approaches. Personally I consider it extremely unlikely that a) US would elect really left leaning president such as Elizabeth Warren and b) would really move away from private prisons any time soon. Having said that, you never know what the general public does and therefore these come with high risk which is at least partly priced in. Very high yield above 10% is also reflecting it as a result. Therefore I bought 80 shares of CoreCivic for 16,17 USD per share and 80 shares of GEO Group for 16,09 USD per share.

Q3/2019 Results

Third quarter is over and this time around it was a bit special one. I decided to restructure my overall finances and paid off my mortgage. This operation involved some stock sales as well since the main motivation was to trim things into a more defensive position (keeping the investment debt carried in portfolio in low end of the allowed range). In global economy main risks are still in place as I expected. Recession risk is real but then again political decisions can easily cause big shifts in a way or another. I might increase cash position in fourth quarter but that remains to be seen. I’m also considering splitting the main portfolio between Nordnet and Nordea. This could be achieved by making additional purchases in portfolio hosted in Nordea.

Third quarter was quite solid considering all the global challenges. Dividend income was 1 337,50 USD and main portfolio value increased 5,45% during the quarter.

Sold: Telia Company, Apple Inc. & NEL ASA

I decided to restructure my finances including mortage. In my current strategy debt to equity ratio is one key metric. I plan to include mortage in the debt component but exclude the attached real estate from equity. This is because co-owned real estate used as home is by no means liquid asset. In theory it doesn’t make sense to pay off cheap loans too soon but there are many factors to it. One is the current cycle phase and trade war in general which makes this likely a decent time to lock in some tax efficient gains and play safe. Therefore I sold today 650 shares of Telia Company for 41,18 SEK per share (roughly break even), 70 shares of Apple Inc for 202,1101 USD per share (roughly 3000 EUR profit plus dividends which I can offset with old losses) and 2500 shares of NEL ASA for 6,68 NOK per share. There’s a good chance that I’ll regret these at least for short term. I still see a 300 USD per share bull case for Apple but then again it’s very much possible that I can buy these back as I expect the trade war issue to remain well beyond US elections next year. NEL is a question mark but I kept 3000 shares just in case my bull thesis for 2025 plays out the way I expect.

Recent Swap: Pfizer for 3M and EPR Properties

Pfizer is about the spin-off it’s generics business and the impact on company profile and dividend strategy remains to be seen. This move is too complex for me understand in detail but I expect further short term pressure on the share price while this saga plays itself out (as many conservative shareholders will wonder how this will play out). I decided to protect the invested capital and sold all 100 shares for 35,44 USD per share (originally bought in the 32,36-33,79 range in 2017). During this time I received 304,00 USD (pre tax) in dividends. I used this capital to buy 10 shares of 3M company for 163,12 USD per share and 20 shares of EPR Properties for 76,77 USD per share. 3M is what it is. Not cheap but acceptable. EPR is a monthly paying REIT which is reasonably recession resistant and should benefit from the insanely low interest rate environment. I might add GEO Group as well since prison REIT should be quite a solid bet going into recession.

Recent Buy: NEL ASA

Just another maintenance purchase. My existing NEL position wasn’t even hundreds so I added to missing 70 shares for 6,975 NOK per share. These small maintenance purchases are mainly done to make sure that I have enough activity on the secondary portfolio to keep the costs down (at least single event for every three months). Other that there’s not much to say about this. I still think the hydrogen mega trend is in the making and NEL is well positioned. It’s a shame that they will probably be bought out eventually but let’s see how long it will take and what kind of terms it will have.