Everything comes to an end eventually. Probably 2020 will not be missed by many. Pandemic is still ongoing concern even though vaccinations are in progress. Even in developed countries the progress seems to be a bit asymmetric and EU in general seems to be lagging behind a bit. US elections were held and results can be considered final even though some aftershocks are still coming. Brexit was also “finalised” but it seems to be a gift that keeps on giving for years to come. In general pandemic together with brexit revealed something fundamental about EU community. As a result of those events I’m slightly more convinced that EU and Euro as currency will start to break down sooner than later. I don’t anticipate it to happen very quickly but quicker than I thought before. This kind of uncontrolled step towards federalization without a real mandate – and for fundamentally incompatible national economies – will eventually bite us in the ass. I’m guesstimating a timeframe of 8-15 years until this really starts to hit us.

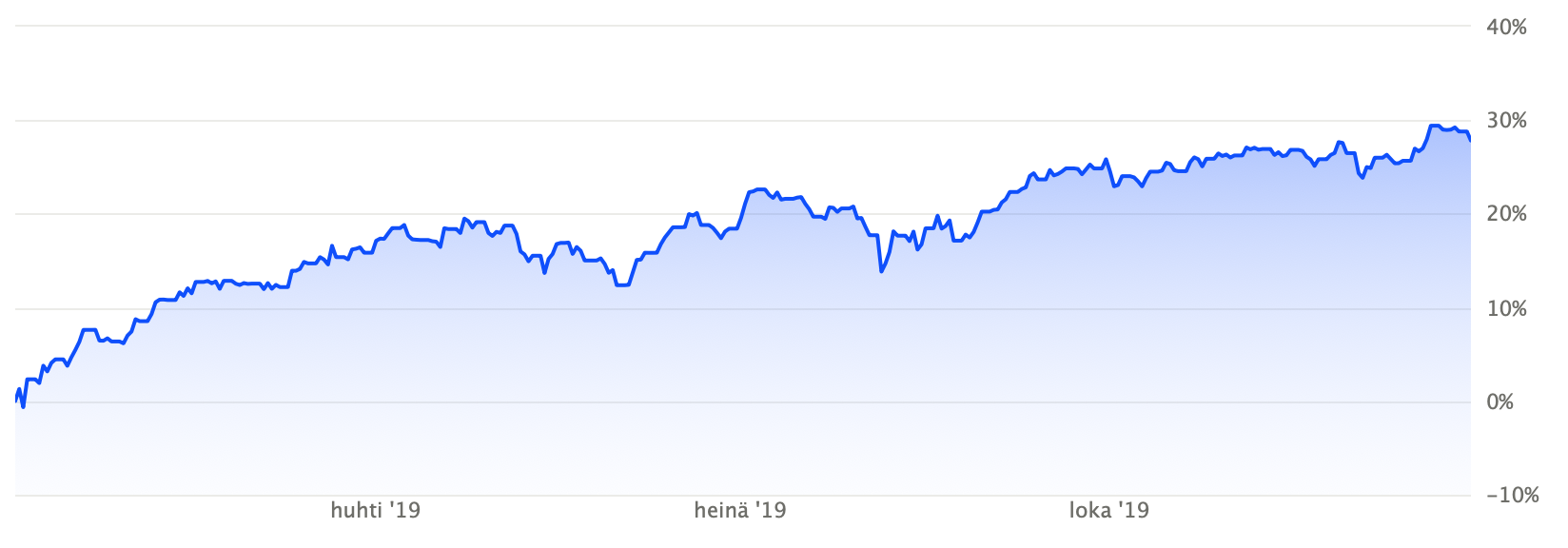

Fourth quarter was somewhat expected kind of quarter. Dividend income compared to previous year was impacted negatively by the pandemic and reduced, eliminated or postponed dividends. Fourth quarter dividend income was 1078,82 EUR before taxes compared to 1 343,74 EUR in 2019. ECB also continued the dividend ban for banks and other financial companies so previously postponed dividends were not paid during this quarter. It is possible that some of those will be paid during 2021 but it’s likely that those and additional since then cumulated profits – buffered dividends if you will – will be heavily capped by ECB. I fear that this ECB decision will be as effective as pissing in your pants in freezing temperatures. FY2020 dividends before taxes were 5040,06 EUR compared to 6769 EUR in FY2019. Primary portfolio market value was hit very hard during the pandemic due to heavy REIT allocation for which recovery is still in progress: 12 month change in dividend portfolio value was −16,43%, fourth quarter change was +6,08% but this paper loss was partially compensated by the secondary growth portfolio.

FY2020 was still a success in personal finances. I tracked my overall savings rate for the whole year and managed to save 73,7% off all my income. That’s a figure which would be hard to beat consistently. I also end the year with portfolio debt to equity ratio of 0,004 which significantly below the 0,1 target average. Plenty of liquidity available for 2021 but in current environment it’s difficult to make any moves. Plan is to keep adding consistently with focus at least on healthcare sector and Swedish dividend stocks. It’s likely that I’ll let cash to to build up a bit but let’s see how the first quarter unfolds.